Hook / Thesis

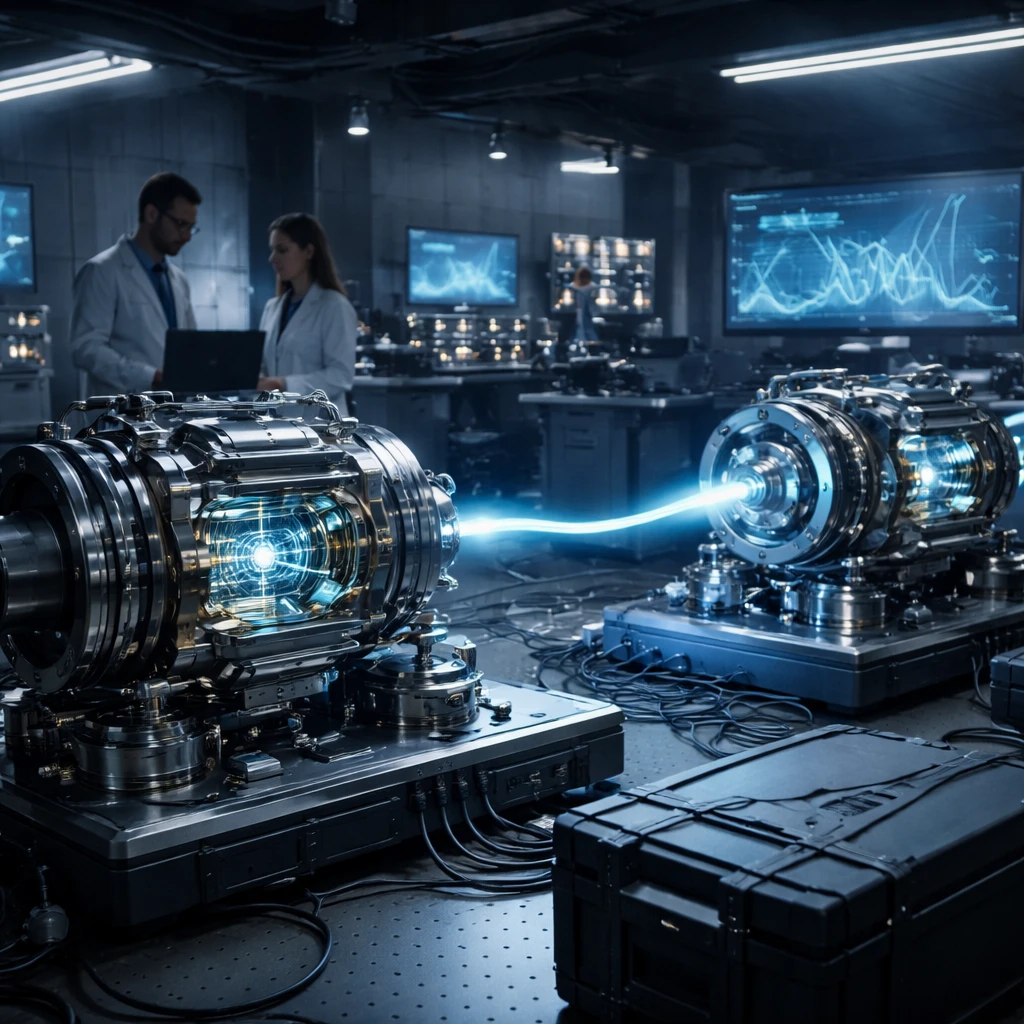

IonQ's recent DARPA HARQ selection and the demonstration of a photonic interconnect linking two independent trapped-ion systems are not academic curiosities - they are the kind of technical and programmatic wins that let investors move from hope to a measurable commercialization pathway. The market is responding: shares rallied sharply, volume spiked, and short-covering pressure is visible. For traders willing to accept meaningful execution and timeline risk, this is a well-defined long opportunity.

My trade thesis is simple: government contracts and a working network demo materially derisk IonQ's path to revenue-bearing systems and services. Combine that with accelerating top-line growth, healthy gross margins and a multi-billion-dollar cash position, and you have the ingredients for an asymmetric trade where the upside can meaningfully outpace the downside if the company converts technology leadership into commercial wins.

What IonQ Does and Why the Market Should Care

IonQ designs and manufactures trapped-ion quantum computers and associated control hardware and interconnects. The commercial case for IonQ rests on two pillars:

- Technology leadership: Trapped-ion qubits have long coherence times and the company has demonstrated photonic interconnects that enable linking multiple quantum systems - a necessary step toward scalable, distributed quantum architectures.

- Commercial pathway: IonQ is moving from a pure-play R&D profile to revenue generation through customers, partnerships and government programs. DARPA selection and Air Force Research Laboratory collaborations represent both validation and potential recurring contract revenue.

Concrete fundamentals

| Metric | Reported / Current |

|---|---|

| Current price | $41.84 |

| Market cap | $15.34B |

| 2025 Revenue | $130.02M |

| 2025 Net Loss | $510.38M |

| Gross margin | 42.06% |

| YoY Revenue Growth | ~428.5% |

| Reported cash | $2.39B |

| Shares short (latest) | ~80.9M (days to cover ~4.5) |

These numbers tell a clear story. Revenue is growing explosively off a small base, and gross margins at roughly 42% show the product economics are meaningful once scale is achieved. Losses are large - $510M in a year - but the company has a multi-billion-dollar cash buffer that gives it runway to execute on DARPA and other contracts. That combination - fast growth, improving unit economics and programmatic revenue - is what can turn a speculative name into a commercially driven equity.

Technicals and market behavior

Technically, momentum is strong: the stock is trading well above its 10- and 20-day SMAs ($30.80 and $30.70) and the 50-day EMA sits near $34.46. RSI is elevated at 71 but the MACD histogram shows bullish momentum, consistent with institutional participation. Volume has spiked well above two-week averages, and high short interest (80.9M) with roughly 3-4 days to cover has magnified intraday moves.

Valuation framing

On a price-to-sales basis the stock trades at an extreme multiple - roughly 100x sales using recent market metrics - which is the market's way of pricing in a long runway to meaningful revenue and dominant market share if IonQ's technology wins. Compare that to conventional hardware or semiconductor businesses where multiples are single-digit to low double-digit; IonQ is being valued more like a high-growth software enterprise with massive future optionality.

That premium can be justified only if quantum computing actually begins to produce recurring, scalable revenue in the next 12-36 months or if IonQ secures further strategic partnerships and government programs that lock in multi-year funding. The DARPA HARQ award and the photonic interconnect demo move IonQ closer to that reality, but investors are still paying for future execution, not current profits.

Catalysts

- DARPA HARQ program advances - milestones, payments, or additional contract awards could trigger re-rating.

- Commercial orders or multi-year agreements from cloud providers, defense contractors or national labs that convert proofs-of-concept into revenue.

- Follow-on technical demonstrations showing scalable entanglement across more nodes - this would further validate the photonic interconnect approach.

- Quarterly results that show sustained revenue growth, margin expansion or a narrowing loss profile.

- Signs of strategic partnering or M&A interest from hyperscalers that want to secure IonQ's trapped-ion IP.

Trade plan - actionable

Trade stance: Long.

Entry price: $41.84 (current market). Target price: $60.00. Stop loss: $32.00.

Horizon: long term (180 trading days). The target assumes continued program execution, at least one visible commercial contract or backlog growth milestone within the next 3-6 months, and broader market risk-on behavior for high-growth hardware names. The stop sits below recent technical support zones and below the 50-day EMA to avoid being stopped out on short-term noise while still limiting downside to a manageable level.

For traders who prefer shorter windows: consider a tactical swing with a shorter stop and the same entry for short term (10 trading days) to capture immediate post-news momentum, or a mid-term (45 trading days) position where you scale in if revenue/backlog updates are positive. I prefer the long-term 180-day approach because converting DARPA and AFRL program wins to commercial revenue takes time and the market can be choppy in the near term.

Risks and counterarguments

- Execution risk: Demonstrations are not the same as scalable, reliable commercial systems. If IonQ fails to translate prototypes into repeatable products, revenue will underwhelm and the multiple can compress quickly.

- Valuation gap: At ~100x price-to-sales, expectations are very high. Any delay in commercialization or downtick in growth could lead to severe downside.

- Competitive pressure: Big tech players and alternate qubit modalities (superconducting, photonic, neutral atom) continue to make progress. IonQ must fend off competitors with deeper pockets.

- Cash burn and dilution: Large annual losses mean the company may need to raise capital if program timing slips, diluting existing shareholders or shifting focus away from long-term R&D.

- Geopolitical / budget risk: Much of the near-term validation is government-driven; defense budgets, program priorities, or contracting delays could slow revenue recognition.

Counterargument: The most credible opposing view is that IonQ's valuation already prices in a near-certain win in the race to commercial quantum computing. If timelines stretch - and they often do for breakthrough hardware - the stock could revert sharply to the downside before the company demonstrates steady, high-margin revenue. That outcome is plausible and is why this trade requires a strict stop.

What would change my mind

I would downgrade this trade if any of the following happen: a) DARPA or other program milestones miss materially and payment schedules slip, b) quarterly revenue growth stalls or gross margins deteriorate, or c) the cash runway is revealed to be shorter than currently expected and the company signals imminent dilution. Conversely, I would add to the position on evidence of multi-year commercial contracts, accelerating ARR-like revenue, or a clear path to margin expansion that materially reduces the current valuation multiple.

Conclusion

IonQ's technical wins and DARPA selection mark a meaningful inflection in narrative risk - from speculative to programmatic. That does not remove execution or valuation risk, but it does give traders a clear, rule-based way to participate. The trade is long with entry at $41.84, a target of $60.00 and a stop at $32.00 on a 180-trading-day horizon. Stay disciplined - respect the stop and watch government program milestones and commercial contract flow as the key value-creation events.

Key points

- IonQ has demonstrated a working photonic interconnect between two trapped-ion systems - a key step toward distributed quantum architectures.

- DARPA HARQ selection provides validation, funding and a clearer commercialization path.

- Revenue is growing rapidly from a small base ($130M in 2025) with gross margins around 42% but losses remain large ($510M in 2025).

- Valuation is extreme (~100x price-to-sales), so execution must follow to justify the current market cap of ~$15.3B.

- A disciplined long with a defined stop and 180-day view captures asymmetric upside while limiting downside if execution falters.