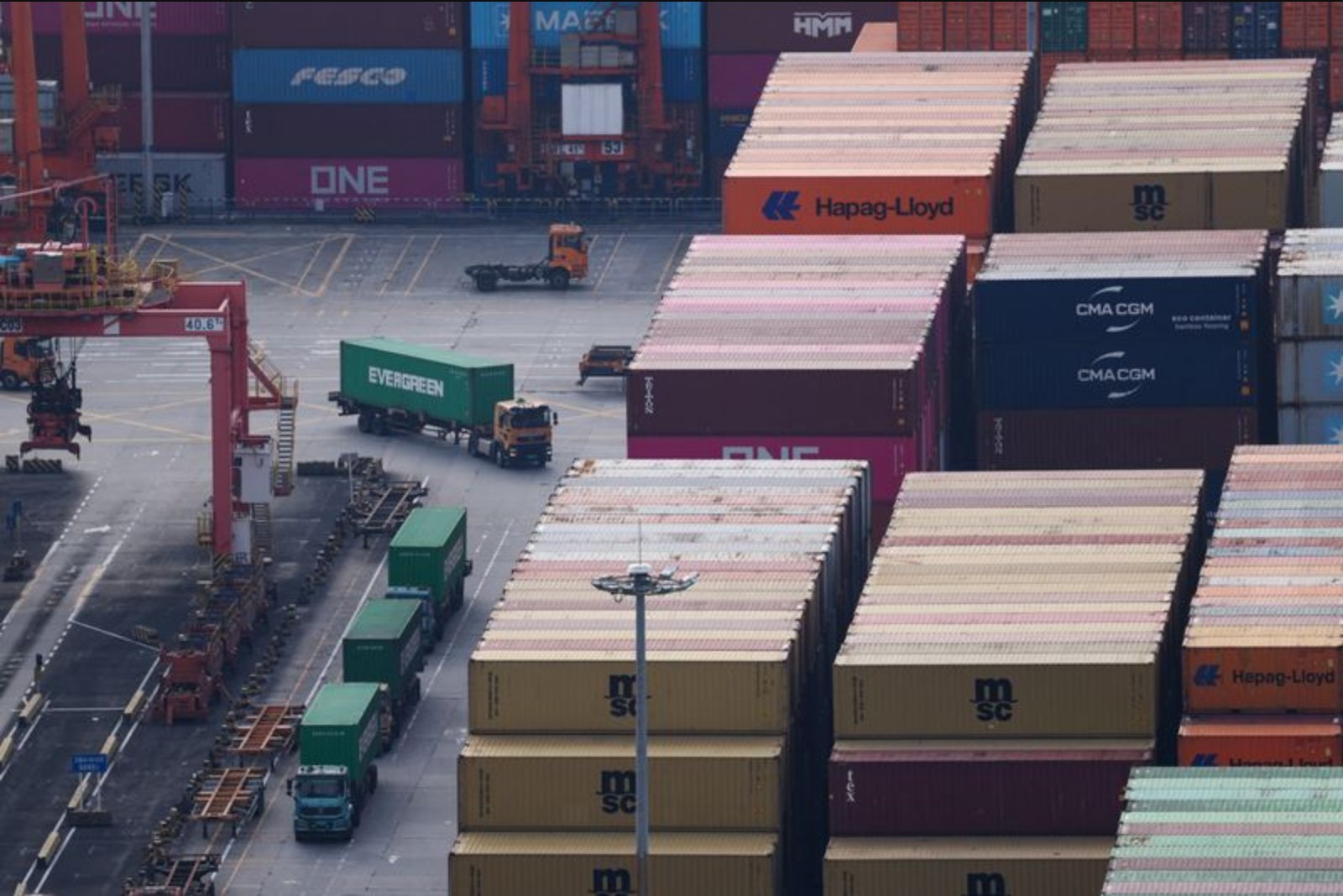

China’s export expansion likely moderated in March as buyers chasing an AI-led demand wave confronted the immediate economic effects of conflict in the Middle East, according to a Reuters poll released on April 13. The poll forecast a year-on-year rise in dollar-denominated exports of 8.6% for March - a notable deceleration from the 21.8% growth recorded in January and February.

The March outcome represents a first substantive assessment of whether global appetite for the chips, servers and related gear that underpin artificial intelligence can offset the negative shock to demand and costs triggered by the Iran war. The conflict has produced an energy shock and renewed market unease associated with past Gulf confrontations, following Iran’s closure of the Strait of Hormuz - the strategic waterway that carries roughly 20% of the world’s oil and gas flows.

China began 2026 with outbound shipments that outpaced forecasts, driven in large part by technology exports. Those strong early-year flows raised the possibility that China could significantly exceed last year’s record trade surplus of $1.2 trillion. But the Iran war has introduced uncertainty over that trajectory by increasing fuel and transport costs and weighing on buyers’ purchasing power.

Even producers that have been criticized abroad for subsidy-supported, low-price manufacturing are not immune to the transmission of higher energy and shipping costs to customers. At the same time, HSBC’s chief Asia economist Fred Neumann noted that lower prices from Chinese suppliers may become more attractive to buyers under pressure, and that decades of commodity stockpiling in China have helped blunt the pass-through of raw-material price shocks to factory gate prices.

Economists polled were divided on how robust Chinese export performance would be in March. Mizuho Securities offered the most bullish projection with a 24% rise, followed by Macquarie Group at 17%. Citigroup was at the low end with a forecast of only 3% growth. A high year-earlier base is also expected to act as a drag after some Chinese factories accelerated shipments a year earlier to beat a U.S. tariff deadline tied to President Donald Trump’s April 2 "Liberation Day" tariff schedule - a dynamic referenced in the poll under the code L1N3QS044.

The Reuters poll also put March imports up 11.2% year-on-year, a slowdown from the 19.8% gain recorded over January and February. External indicators of Chinese demand showed strong flows into the country, with South Korea’s exports to China increasing 62.4% in March; that rise was driven in part by a 151.4% surge in global semiconductor shipments tied to higher memory prices and persistent AI-driven server demand.

Chinese factory activity data for March suggested that goods exports continued to contribute to growth, but that the Iran war had depressed sentiment as commodity prices jumped, raising input costs for manufacturers. On a trade-balance basis, the poll forecast China’s surplus would narrow to $108 billion in March from $214 billion over January and February.

Separately, the poll noted a planned visit by U.S. President Donald Trump to China in May for talks with President Xi Jinping. That trip could yield gains in specific areas such as farm trade and airplane parts, though the poll reflected a view that it was unlikely to ease deep strategic tensions, particularly on the subject of Taiwan.

What this means for industry and markets

- Technology and semiconductor supply chains remain central to China’s export strength, but rising energy and transport costs could compress margins and slow shipment momentum.

- Commodity-sensitive sectors and logistics-intensive manufacturers face higher input and freight costs that may temper global buyers’ purchasing power.

- Trade flows and policy developments, including high-profile diplomatic meetings, could deliver targeted opportunities in agriculture and aircraft parts even as broader strategic rifts persist.